As we enter the second quarter of 2026, historically the highest selling season of the year, let’s look back on the first quarter data to get a read on the market and develop our forecast.

The first quarter was steady, selective, and gaining strength. The number of new listings dropped sharply, down 18.07% year over year, while the median price rose 11% year over year to $1.24 million. With fewer properties entering the market, well-priced homes are facing less competition and attracting more focused attention. For sellers, this is creating a clear advantage. The increase in median sale price was a strong signal that buyers are still willing to move forward when value aligns with expectations. This is not a market lacking demand - it is one where buyers are thoughtful, but ready to act when the right property appears. The restricted inventory resulted in the number of contracts signed down 5.5% year over year during the first quarter.

New development tells a similar story, with an added layer of confidence. Average prices increased 23% year over year to $5.4 million, while contract activity remained stable compared to Q1 2025. The combination of rising prices and steady deal flow points to buyers prioritizing quality and long-term value, particularly in buildings offering innovative desirable design, amenities, and overall lifestyle appeal.

On the financing side, the backdrop is gradually improving. Mortgage rates averaged 6.38% this week, down from 6.65% a year ago. While there has been some volatility, both purchase and refinance applications are up year over year, showing that buyers are adjusting to current conditions rather than waiting on the sidelines. Federal Reserve Chair Jerome Powell said Monday that he sees inflation expectations as grounded despite rising energy prices, implying the Federal Reserve will not need to respond with higher interest rates.

At the same time, broader financial market strength continues to support real estate demand. Wall Street’s 2025 bonus pool reached a record $49.2 billion, up 9% from 2024, while pretax profits for New York–based broker-dealers surged 30% to $65.1 billion, the highest level on record. Historically, this level of compensation has translated directly into increased activity in the high-end Manhattan housing market.

For sellers, the second quarter spring market offers a real opportunity to stand out in a less crowded landscape. For buyers, success comes down to preparation and timing, especially as quality properties continue to move quickly.

The Spring market forecast is to expect more buyers entering the market as:

-

Continued strength in Wall Street compensation, which historically fuels demand in the luxury Manhattan market.

-

Renewed interest in real estate as a stable asset amid stock market volatility and broader geopolitical uncertainty.

-

The ongoing shift back to in-office work, particularly across financial services, legal, and insurance sectors, bringing renewed focus to New York City living.

In this market climate, having a clear strategy makes all the difference. If you are thinking about selling or purchasing, I would be happy to help you navigate the market and position you to take full advantage of the opportunities ahead.

All my best,

Iman Bacodari

The Bacodari Team

(646) 226-6084

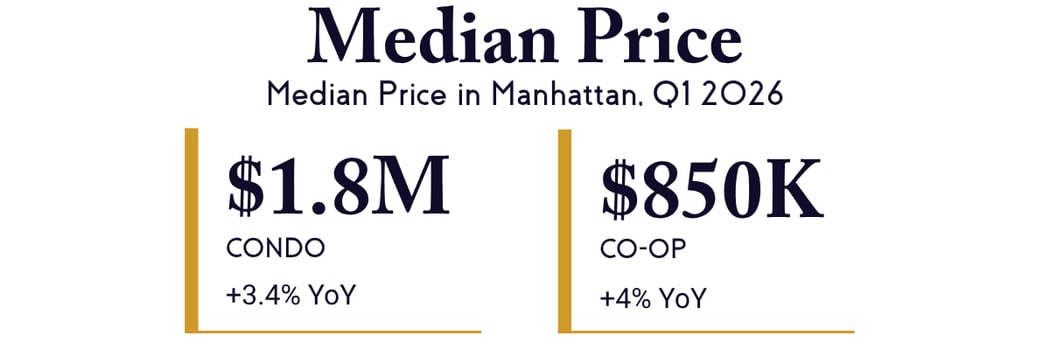

In Manhattan, condos saw 984 contracts signed (down 5% year over year), while co-ops recorded 1,282 contracts signed (down 8%), pointing to a slightly sharper pullback in co-op activity.

Median prices moved higher across both segments, with condos reaching $1.8M (+3.4%) and co-ops at $847K (+4%), showing steady pricing.